Student loans are a reality for millions of individuals pursuing higher education. While they provide the necessary funds to finance education, repaying them can be a daunting process. With various repayment plans available, choosing the right one can significantly impact your financial well-being. This comprehensive guide will help you understand and navigate student loan repayment plans effectively.

Understanding Student Loans

Before diving into repayment plans, it’s essential to understand the different types of student loans available. There are two primary categories:

- Federal Student Loans – These loans are funded by the U.S. Department of Education and typically offer more flexible repayment options.

- Private Student Loans – These are issued by banks, credit unions, and other private lenders. They generally have stricter repayment terms and fewer forgiveness options.

Each loan type has distinct features, including interest rates, repayment terms, and eligibility for forgiveness programs.

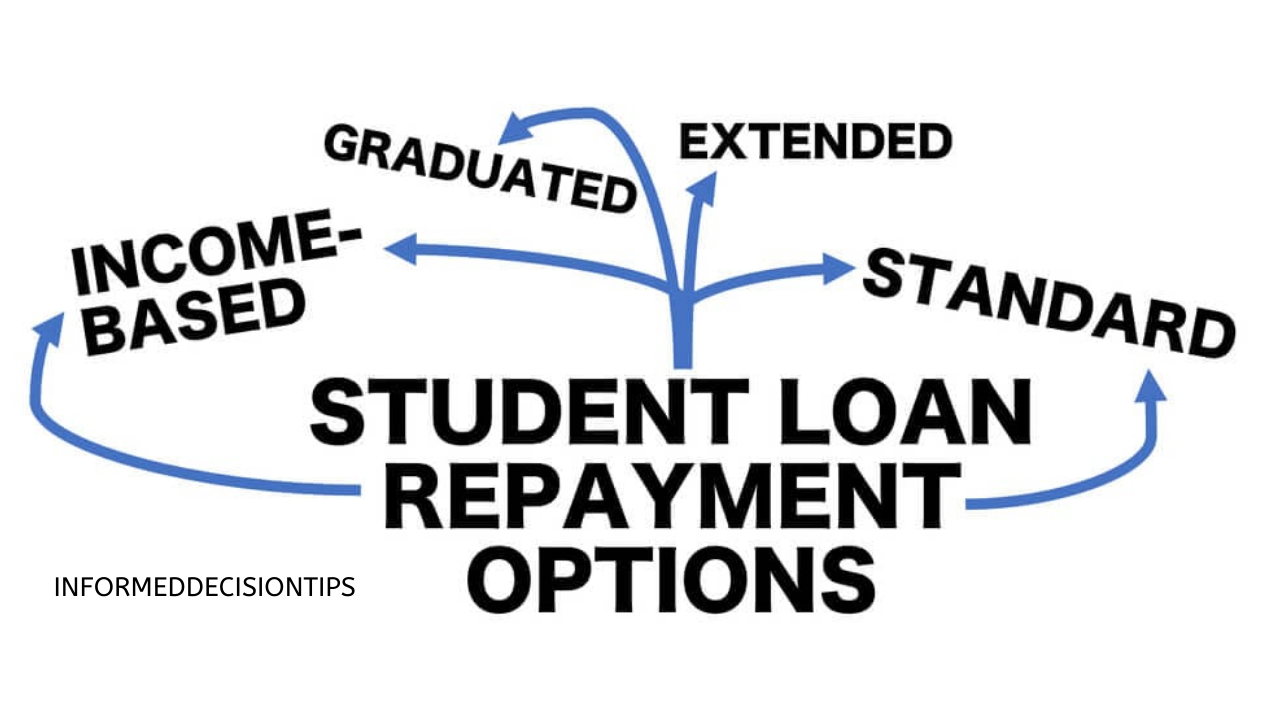

Federal Student Loan Repayment Plans

The U.S. Department of Education offers several repayment plans for federal student loans. Choosing the right plan depends on factors such as income, loan balance, and financial goals.

1. Standard Repayment Plan

- Description: Fixed monthly payments over ten years.

- Best for: Borrowers who want to pay off loans quickly and minimize interest payments.

- Pros:

- Lower interest paid over time.

- Loan is paid off faster.

- Cons:

- Higher monthly payments may not be affordable for everyone.

2. Graduated Repayment Plan

- Description: Payments start low and increase every two years over ten years.

- Best for: Borrowers expecting their income to rise over time.

- Pros:

- Lower initial payments ease the financial burden.

- Cons:

- Higher overall interest paid compared to the Standard Plan.

- Payments increase regardless of actual income growth.

3. Extended Repayment Plan

- Description: Fixed or graduated payments over up to 25 years.

- Best for: Borrowers with large loan balances who need lower monthly payments.

Why Financial Independence is Important and How to Achieve It

- Pros:

- More manageable payments.

- Cons:

- More interest paid over time.

- Not eligible for loan forgiveness.

4. Income-Driven Repayment (IDR) Plans

These plans base monthly payments on a percentage of discretionary income and extend the repayment term to 20-25 years. Any remaining balance after this period is forgiven.

Income-Based Repayment (IBR)

- Payments: 10-15% of discretionary income.

- Forgiveness: After 20-25 years.

- Best for: Borrowers with high debt relative to income.

- Pros:

- More affordable payments.

- Cons:

- More interest paid over time.

Pay As You Earn (PAYE)

- Payments: 10% of discretionary income.

- Forgiveness: After 20 years.

- Best for: Recent graduates with low starting incomes.

- Pros:

- Lower payments based on income.

- Cons:

- Must have a partial financial hardship.

Revised Pay As You Earn (REPAYE)

- Payments: 10% of discretionary income.

- Forgiveness: After 20 years (undergraduate loans) or 25 years (graduate loans).

- Best for: Borrowers with fluctuating income.

- Pros:

- Interest subsidies help prevent balance growth.

- Cons:

- Payments increase if income rises.

5. Income-Contingent Repayment (ICR)

- Payments: The lesser of 20% of discretionary income or fixed payments over 12 years.

- Forgiveness: After 25 years.

- Best for: Parent PLUS loan borrowers.

- Pros:

- More flexible than standard plans.

- Cons:

- Higher monthly payments compared to other IDR plans.

Private Student Loan Repayment Plans

Private lenders do not offer the same flexible repayment options as federal loans. However, options may include:

- Fixed or variable interest rates

- Shorter or extended repayment terms

- Forbearance or deferment options in hardship cases

- Loan refinancing for lower interest rates

Choosing the Right Repayment Plan

Consider the following factors when selecting a repayment plan:

- Income Level – If your income is low, an IDR plan may be a better fit.

- Loan Balance – Larger balances might benefit from extended repayment or refinancing.

- Financial Goals – If you want to be debt-free quickly, the Standard Plan is best.

- Eligibility for Forgiveness – IDR plans offer loan forgiveness after 20-25 years.

- Interest Costs – The longer the repayment term, the more interest you will pay.

Loan Forgiveness and Assistance Programs

Several programs help reduce or eliminate student loan debt:

- Public Service Loan Forgiveness (PSLF): Forgives federal student loan debt after ten years of qualifying payments for those in government or nonprofit jobs.

- Teacher Loan Forgiveness: Offers up to $17,500 in forgiveness for teachers working in low-income schools.

- State-Based Forgiveness Programs: Some states offer assistance for specific professions.

- Employer Repayment Assistance: Some employers provide student loan repayment benefits.

Refinancing and Consolidation

- Loan Consolidation: Combines multiple federal loans into one, simplifying repayment but potentially increasing interest costs.

- Refinancing: Allows borrowers to replace existing loans with a new one at a lower interest rate, typically through private lenders.

- When to Refinance: If you have good credit and a stable income, refinancing can lower interest rates and monthly payments.

Managing Repayments Effectively

To stay on top of your student loans:

- Set Up Auto-Pay – Many lenders offer interest rate discounts for automatic payments.

- Budget Wisely – Include loan payments in your monthly financial plan.

- Make Extra Payments – Paying more than the minimum reduces interest and loan term.

- Monitor Loan Servicers – Stay informed about your loan status and servicer policies.

- Seek Assistance – If struggling with payments, explore deferment, forbearance, or alternative repayment plans.

Navigating student loan repayment plans requires careful consideration of your financial situation and long-term goals. Whether choosing a standard plan, income-driven repayment, refinancing, or seeking loan forgiveness, understanding your options empowers you to make the best decision for your financial future. By staying informed and proactive, you can successfully manage and ultimately eliminate student loan debt.

Leave a Reply